In my first article for Tranglo, I discussed fintech’s role in promoting financial inclusion. Since then, I’ve understood more what financial inclusion means to me personally.

So, when Bank Negara Malaysia published the second and latest Financial Inclusion Framework (2023-2026) in June, I took a long look at it, and here is my digest.

Digitalising people

One of the most important tools for enhancing inclusion, according to BNM’s framework, is digital financial services (DFS). These services, often provided by financial institutions, non-financial institutions and financial technology companies, have seen a surge in adoption in Malaysia circa 2020.

We can attribute this growth to the pandemic’s influence and government programmes. For example, the e-Tunai and e-Penjana initiatives disbursed monetary aid into eWallets, such as Touch ‘n Go, Boost and GrabPay, resulting in the e-wallet usage rate increasing to 57%, doubling the rate before 2020.

I also started using the Touch ‘n Go eWallet to benefit from e-Penjana during this time. You could say I was a forced convert - with the pandemic driving merchants to prefer cashless transactions - but I have no regrets!

However, the connection between government initiatives and financial inclusion might not immediately be apparent to many, including yours truly, only becoming clearer upon examination.

By fostering an environment for digital wallets to thrive with fewer restrictions and easier sign-ups, the government has opened financial access to underserved individuals and small businesses lacking access to traditional financial institutions.

Delivering results

In the 2022 Global Financial Inclusion Index by the Principal Financial Group, Malaysia was ranked the 20th most financially inclusive of 42 markets. The top 5 countries were Singapore, the United States, Sweden, Hong Kong and Finland.

Notably, Malaysia ranked 5th for financial inclusion support for employees, with the country’s financial system also receiving high scores for enabling business confidence and prioritising consumer financial protection.

These achievements were not coincidental. The government’s efforts to establish infrastructure, combined with fintech companies’ innovations, have paved the way for the widespread use of DFS. Surveys highlight that around 74% of Malaysians use DFS, and the World Bank’s 2021 Global FINDEX Report indicates that 79% of Malaysian adults engage in digital payments, with 42% adopting them for the first time during the pandemic.

A bit on the history of financial inclusion frameworks in Malaysia

Malaysia’s journey towards financial inclusion began with the Financial Inclusion Framework 2011-2020. This initiative improved access to basic financial services and financial literacy. A few improvements include higher populations living in sub-districts with physical access to financial services (82% in 2011 to 99% in 2020) and higher e-payment usage among adults (63% in 2014 to 79% in 2021).

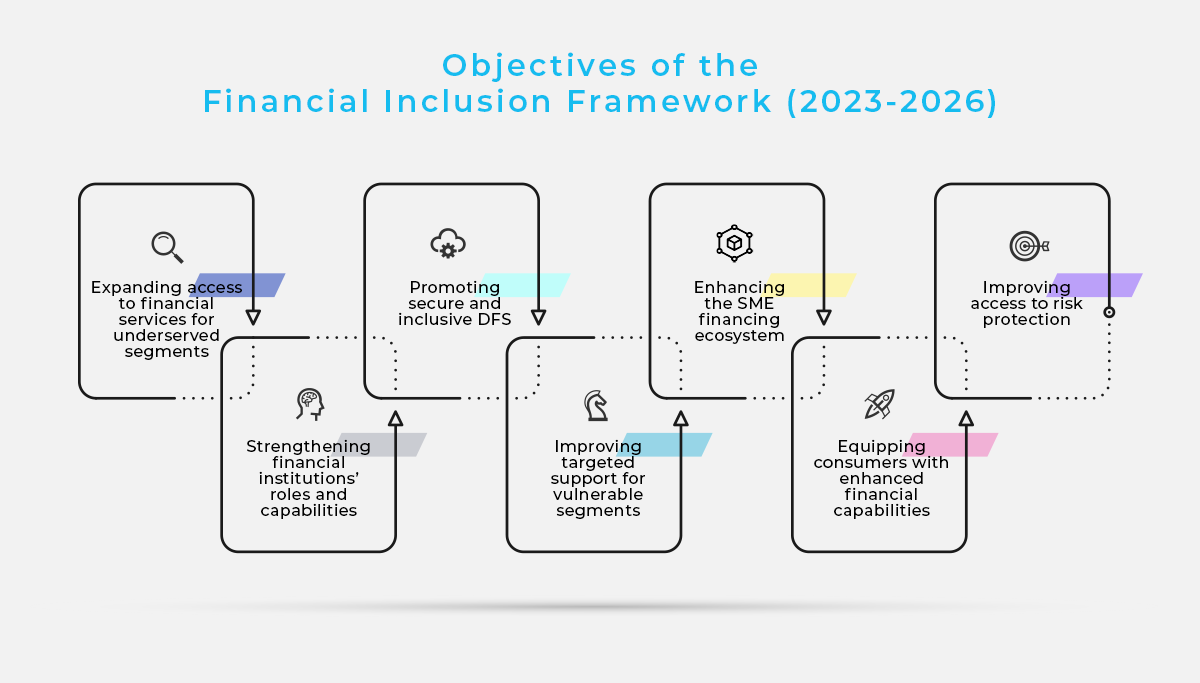

Despite these achievements, challenges persist, prompting Bank Negara to develop the current framework that is the focus of this article. I won’t bore you with too many details, but there are 7 clear objectives.

According to the framework, improving financial inclusion is a key priority under the 12th Malaysia Plan 2021-2025. While the aim is to ensure Malaysians have access to quality and affordable financial services, the focus is on delivering them via innovative and technology-led solutions, which leads us back to digital financial services 😉.

Financial literacy = financial inclusion

Lastly, individuals must know their pivotal role in promoting financial inclusion and not rely solely on government efforts and initiatives.

In this respect, we can improve our financial literacy by perusing online information. Educating ourselves through reading, consuming multimedia content like podcasts, and getting the advice of financial experts can enhance our ability to seek financial services, manage finances and make informed decisions. After all, when someone wants to include us, we must try to be included.

I don’t know about you, but I think I’m much more financially literate and included now. 😂