In January 2023, Juniper Research predicted that global B2B cross-border payments will exceed USD 40 trillion by 2024, a 9% increase from USD 37 trillion in 2022. The United Kingdom-based company attributes the rise to eCommerce marketplaces' rising popularity.

Cross-border payment development and trends have evolved as a result of the convergence of technology and functionality. However, fundamental problems remain. Despite the surge of digital payments, sections of payment rails remain encumbered by legacy systems that are slow and expensive.

Cross-border payment challenges

The World Bank stated that, on average, a sender pays 6.4% of the transfer value for a cross-border transaction. This is a hefty price, particularly for migrant workers who wish to send money back home to their families or micro or small businesses to expand their global market.

Another challenge is transparency, which is crucial to avoid unintended cost consequences of data provision. Lack of transparency in cross-border payments happens as layers of intermediaries happen during the process. One of the reasons that caused this is the remittance fee structures as services charges, and foreign exchange trade occurs during the process, which leads to uncertainty.

For example, Wise exposed that Europeans lost € 12.5 billion in hidden fees when sending money out of the continent in a year because of exchange rate mark-ups.

Locked-up capital is also preventing businesses from making gains in cross-border payments. A 2019 Quickbooks survey found that 61% of small businesses face persistent cash flow problems. Most cross-border payments work on the pre-funding of accounts for settlement, which means, right now, banks either must invest in liquid assets that can be used as collateral or have adequate liquidity in a foreign central bank or in their correspondent bank account to settle the payment.

Addressing cross-border payment challenges

Authorities in different regions are making cross-border payments faster and easier, even if the progress is slow. For example, a landmark regulation – Cross-Border Payments Regulation 2 - was implemented in Europe in 2020 to compel banks to disclose “hidden fees”.

In Southeast Asia, the central banks of Malaysia, Indonesia, Singapore, Thailand, and the Philippines signed a Memorandum of Understanding on Cooperation in Regional Payment Connectivity in November 2022 to strengthen and enhance cooperation on payment connectivity to support faster, cheaper, more transparent and more inclusive cross-border payments.

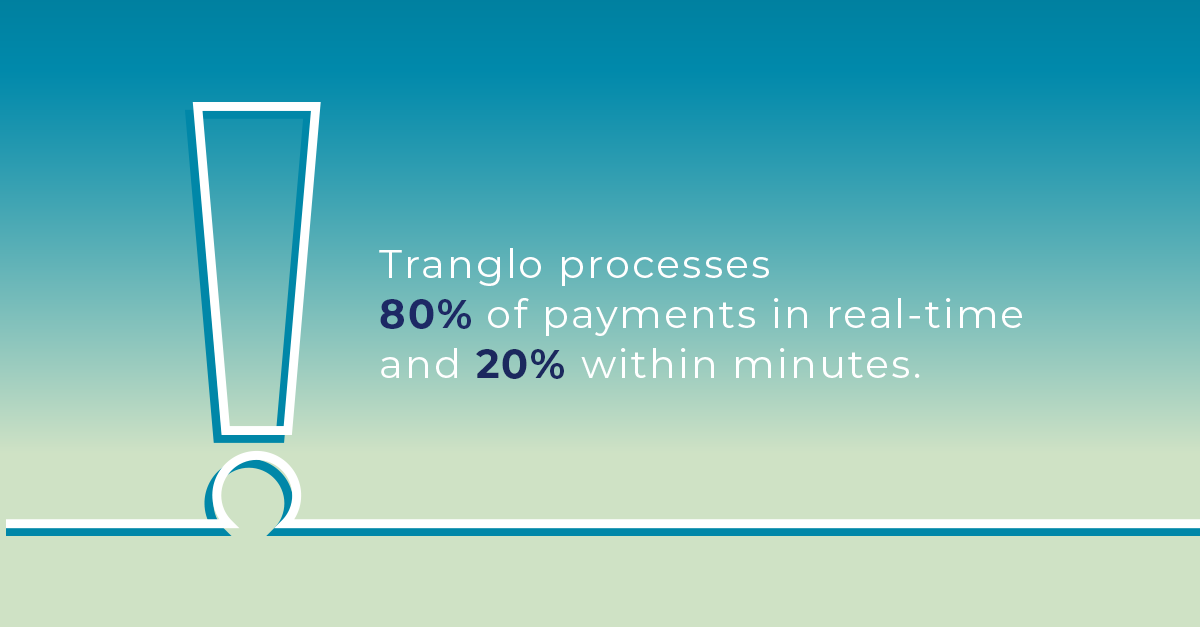

Fintech cross-border payment providers have also emerged to overcome these challenges through non-bank partnerships. Tranglo, for example, has established regional partnerships with non-bank entities and other financial institutions in key corridors. This strategy has been successful, with Tranglo processing 80% of payments in real time. This significantly improved over the global average processing time of 2-5 days.

Ripple, the US-based leading provider of crypto solutions for businesses, introduced On-Demand Liquidity in 2018, a crypto solution to ease frictions associated with “low value, high volume” cross-border payments like remittances. Hai Ha Money Transfer managing director Dianne Nguyen said Ripple’s ODL had helped to solve pre-funding and speed of fund settlement.

Cross-border payment development, as explained above, focuses on faster and more affordable transactions, increased transparency and improved security. In the meantime, the adoption of new technologies and new payment standards drives trends.

So, what are some cross-border payment development and trends in 2023?

More regional partnerships than ever before

More countries will integrate their payment systems to make domestic and cross-border payments easier and faster for users. For example, Malaysian and Singaporean tourists can now pay for goods and services using preferred e-wallets when they are travelling in these countries by just scanning QR codes developed by the respective countries’ central banks. This follows a similar arrangement between Singapore and Thailand in 2021. In another development, Indian tourists can soon use digital wallets in Nepal.

Watch out for Apple and Google’s take on mobile payments

In a 2023 interview, Alipay+ European Head of Business Development Pietro Candela said, “businesses should be looking to options that allow customers to complete a transaction inside an app, instead of on a plastic card or NFC touchpoint”. Candela said this mobile-first strategy would be imperative in creating a seamless and connected payment experience.

Mobile wallets can be integrated into multiple ecosystems, from e-commerce to a larger network of other businesses, providing various financial services. Both technology giants in the US, such as Apple and Google, have reportedly been building out payment offerings as part of their super apps and local players.

AI post-ChatGPT is a serious business

Artificial intelligence (AI) has been a matter of discussion for years, and it became the talk of the town after ChatGPT, an AI chatbot, was introduced. Last year, IBM research found that usage of AI is becoming more prevalent in all industries globally with 35% of businesses reporting using AI; Nvidia revealed that 37% of financial service companies plan to use AI.

In cross-border payments, AI can make things easier, faster, and safer. AI helps predict FX rates more accurately and helps to process transactions in real time with transparent costs for all parties. AI expedites transactions as it can read data and spot things humans often neglect. It can develop better options that meet customers’ needs, hence, better customer service. It can also be automated to detect fraud or compliance-related offences such as money laundering or terrorism financing.

Can CBDCs come of age with help?

In a November 2022 speech, International Monetary Fund deputy managing director Bo Li mentioned multilateral cross-border payment platforms that combine new forms of central bank digital currency (CBDC) with the latest technology. These platforms will shorten transaction chains and improve security as central bank money is available for settlement. Such a system can also make compliance checks easier without compromising data sovereignty in each country.

The cross-border payment industry can look at bringing this innovation and collaborating with the public sector in 2023. As of March 1, 65 countries are in the advanced stage of CBDC development, and over 20 central banks have launched their pilots, including China, Japan, India, the UK and the US.

Leading the way

The industry is evolving, and several cross-border payment development and trends have emerged in 2023 to transform the industry. Fintech providers are leading the way in addressing the challenges of cross-border payments and are well-positioned to take advantage of the opportunities that lie ahead.